Pembina Pipeline Corporation

- 11 minutes ago

- 9 min read

Summary:

Attractive valuation upside from strategic transactions:

The two proposed deals represent meaningful near-term catalysts for PPL’s share price, with the base case analysis indicating incremental value of approximately $10.80 to $14.12 per share based on current market multiples. The modeled assumptions incorporate potential ownership upside through optionality, resulting in a slightly higher effective ownership stake than the stated base case.

Stable infrastructure cash flow profile with potential margin upside:

The pipeline opportunity involves a mature, long-haul crude transportation asset supported by long-term, fee-based or take-or-pay contracts. Given the asset’s high operating leverage, low variable costs, and limited commodity price exposure, EBITDA margins could be materially higher than the base case assumption. Sensitivity cases incorporating 80% and 90% asset EBITDA margins demonstrate additional potential upside.

Strategic portfolio benefits and geopolitical positioning:

Beyond direct valuation upside, the transactions provide exposure to critical Canadian infrastructure and an emerging data infrastructure opportunity outside the U.S. market. The projects may also serve as a strategic hedge against U.S.–Iran-related geopolitical risks, as heightened tensions could accelerate Canadian support for domestic energy infrastructure expansion. While timing remains uncertain, the underlying strategic rationale supports a high probability of advancement.

The Research

A prevailing theme is emerging in recent press coverage, especially concerning data center infrastructure developments and agreements, mainly by major U.S. technology companies aiming to construct the infrastructure needed to meet the growing demand for artificial intelligence and its supportive role.

Another theme is the increasing geopolitical risk, especially related to the fluctuations in crude oil supply, primarily driven by the ongoing and intermittent conflicts between the U.S. and Iran.

Prudent investors are likely seeking ways to increase their exposure to one theme while mitigating their exposure to the other. We believe that Pembina Pipeline Corporation (TSX: PPL) offers a compelling opportunity to achieve both within a single investment.

To provide broader context for these recent developments, we discuss two key catalysts. First, in July 2026, Pembina Pipeline Corporation reached a final investment decision (FID) to proceed with the Greenlight Electricity Centre project in Alberta. Second, the Canadian federal government and the Government of Alberta recently announced their support for developing a new crude oil pipeline connecting Alberta to Canada's Pacific Coast.

Greenlight Electricity Centre

Pembina Pipeline Corporation's final investment decision (FID) on the Greenlight Electricity Centre marks one of the company's largest growth investments and represents a strategic expansion beyond its traditional midstream business into power infrastructure supporting artificial intelligence (AI) and hyperscale data centres. Announced on July 2, 2026, the project will be developed through a partnership between Pembina (47.5%), Morgan Stanley Infrastructure Partners (47.5%), and Kineticor Asset Management (5%). The facility will be located in Sturgeon County, Alberta's Industrial Heartland, and will supply dedicated, behind-the-meter electricity to a major data centre customer under a long-term contracted arrangement. Commercial operations are expected to begin in the second half of 2030.

The first phase of Greenlight consists of a 932-megawatt, natural gas-fired combined-cycle power plant designed to deliver reliable, around-the-clock electricity using high-efficiency gas turbines that recover waste heat to generate additional power through a steam turbine. The project addresses the rapidly growing electricity demand driven by AI computing and cloud infrastructure while leveraging Alberta's abundant natural gas resources. The project has also been designed with scalability in mind, with permits and site capacity that could support future expansion as data centre demand continues to grow.

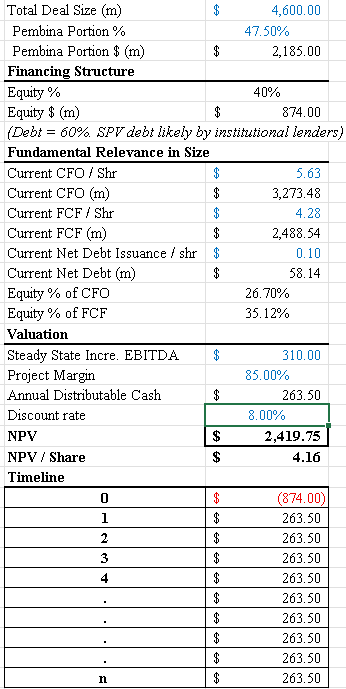

The total project cost is estimated at approximately C$4.6 billion, including financing costs during construction. Pembina's gross share amounts to roughly C$2.3 billion, although its net investment is expected to be approximately C$2.1 billion after accounting for roughly C$190 million of proceeds from the sale of land to the data centre customer. Once operational, the project is expected to generate approximately C$310 million of annual run-rate adjusted EBITDA attributable to Pembina, providing a significant source of long-term, fee-based cash flow that supports the company's target of 5% to 7% annual adjusted EBITDA per share growth through 2030.

Strategically, Greenlight extends Pembina's integrated energy value chain by creating incremental demand for Western Canadian natural gas and natural gas liquids, which in turn can increase utilization across the company's existing gathering, processing, transportation, and storage assets. Beyond the direct earnings contribution from the power facility, the project positions Pembina to participate in Alberta's emerging AI infrastructure ecosystem, where reliable power supply has become a critical competitive advantage. Management has indicated that Greenlight could serve as the foundation for a scalable new business line, with additional power-to-data centre developments and a potential second phase already under evaluation.

Pipeline Expansion

The proposed West Coast oil pipeline represents one of Canada's most significant energy infrastructure initiatives in decades and is designed to materially expand the country's crude oil export capacity to global markets. Announced jointly by the Canadian federal government and the Government of Alberta in July 2026, the project envisions constructing a new pipeline capable of transporting more than one million barrels of crude oil per day from Alberta to British Columbia's southern Pacific Coast. The pipeline would largely follow the existing Trans Mountain corridor before connecting to a new export terminal, allowing Canadian producers to diversify exports beyond the United States and strengthen access to high-growth Asian markets. Construction could begin as early as September 2027, subject to expedited regulatory approvals, Indigenous consultation, and environmental permitting.

Unlike previous privately led pipeline proposals, the project is backed directly by both levels of government. The federal and Alberta governments will serve as the majority owners, while Pembina Pipeline Corporation will hold a 10% ownership interest during construction and contribute its engineering, construction, and operational expertise. The ownership structure also reserves an equity interest for Indigenous communities, reflecting a greater emphasis on Indigenous participation compared with previous pipeline developments. The proposal forms part of a broader nation-building strategy intended to enhance Canada's energy security, improve export competitiveness, and reduce reliance on U.S. demand amid evolving global trade dynamics.

Strategically, the pipeline would alleviate long-standing egress constraints facing Western Canadian producers by creating substantial new export capacity to tidewater. Greater access to international markets is expected to improve pricing for Canadian crude by narrowing the discount between Western Canadian Select (WCS) and global benchmark prices, while supporting future production growth from the oil sands. For Pembina, participation in the project further strengthens its position within Canada's energy infrastructure network and creates opportunities to generate long-term earnings through its ownership stake, construction activities, and the increased demand for its broader gathering, transportation, storage, and terminal assets resulting from higher crude production and export volumes.

Framework & Calculations

Throughout the rest of this research, we aim to combine these two deals and ultimately translate them into quantifiable accreitve impact to Pembina's share price with the framework provided below.

Framework

Greenlight Data Centre

We will first apply a Net Present Value (NPV) framework under a going-concern assumption to estimate the potential quantifiable value creation for Pembina at the equity level and assess the financial rationale for proceeding with the Greenlight Data Centre infrastructure build.

The analysis begins by forecasting the project’s long-term operating earnings, which are expected to be relatively stable due to the presence of a long-term contractual arrangement with the co-located data centre, reducing exposure to volatile wholesale electricity market prices. Operating costs are incorporated using an assumed project EBITDA margin of 85%, which represents our base-case estimate based on industry research and project characteristics. Pembina’s economic entitlement is then calculated based on its 47.5% ownership interest in the joint venture, representing its share of the project’s equity-level cash distributions.

The discount rate applied in the valuation is assumed to be 8% in nominal terms, reflecting the project’s contracted infrastructure profile and capital structure. The relatively lower discount rate is supported by the predictable nature of contracted cash flows, project-level financing, and reduced commodity price exposure compared with merchant power generation assets. The resulting NPV represents the present value of Pembina’s expected future equity cash flows relative to its required equity investment, providing an estimate of the value created for Pembina shareholders from the Greenlight investment.

Finally, the estimated NPV is translated into a per-share value impact by dividing the total value creation attributable to Pembina by the company’s projected end-of-period shares outstanding. This incremental value per share is then added directly to our reference share price, defined as Pembina’s closing stock price on July 2nd, to derive the implied value impact of the Greenlight Data Centre investment on the company’s equity valuation.

Pipeline Expansion

The valuation framework for a new crude export pipeline should be built from the bottom up, starting with the physical capacity of the asset and translating operating economics into enterprise value. The first step is estimating annual throughput, which is calculated as pipeline capacity multiplied by days in operation (for example, a 1 million barrel per day pipeline generates approximately 365 million barrels per year at full utilization). The next step is applying a comparable pipeline toll rate, expressed as dollars per barrel, which represents the fee paid by producers to transport crude. The appropriate toll assumption is derived from comparable export pipelines such as Trans Mountain, with adjustments for route length, construction cost, regulatory structure, contracted volumes, and utilization. For a large Alberta-to-Pacific export pipeline, a reasonable long-term toll range would typically be benchmarked against similar export infrastructure rather than domestic gathering systems.

Annual pipeline revenue is then calculated as throughput multiplied by the toll rate. EBITDA is derived by applying an asset-level pipeline EBITDA margin, reflecting the high operating leverage of fee-based infrastructure assets. Unlike upstream producers, pipelines generally have low variable operating costs, resulting in structurally higher EBITDA margins. Once incremental EBITDA is estimated, the value of the pipeline asset is calculated using an EV/EBITDA multiple based on comparable publicly traded midstream companies and recent infrastructure transactions. The implied enterprise value is then adjusted for ownership percentage to determine the value attributable to the specific investor, such as Pembina’s 10% ownership interest. Finally, the incremental equity value is divided by shares outstanding to estimate the potential impact on per-share valuation.

Calculation

Greenlight

We also assess the relative magnitude of Pembina's equity funding requirement by comparing its expected equity contribution to the company's most recent annual cash flow from operations (CFO) and free cash flow to equity (FCFE). This analysis indicates that, while the investment represents a meaningful capital commitment, it remains manageable relative to Pembina's existing cash-generating capacity and is therefore unlikely to place significant pressure on the company's ongoing operations or financial flexibility.

It is also important to note that project-level debt financing is excluded from the initial investment assumptions. Under the Greenlight project's financing structure, approximately 60% of the total construction cost is expected to be financed through debt raised by the project's special purpose vehicle (SPV), rather than by Pembina directly. As a result, Pembina's upfront capital commitment consists primarily of its proportionate equity contribution to the joint venture, while the project debt is expected to be serviced by the project's future operating cash flows. Accordingly, the valuation compares the present value of Pembina's future equity cash flows with its required equity investment, rather than the project's total construction cost.

Pipeline Expansion Valuation

As discussed in our framework, we assumed a toll fee ranging from $12 to $18 per barrel of crude oil, with a base asset EBITDA margin of 70%. While the stated project ownership stake is 10%, we incorporated the optionality of a potential increase to a 15% ownership stake, with an assumed probability of 20%. As a result, the modeled ownership stake is marginally higher than the stated base case. Please also note that the model snapshot provided above includes the previously discussed Greenlight project as well.

Based on the latest market trading multiples, we estimate that this transaction could contribute incremental value ranging from $10.80 to $14.12 per share under the base case scenario.

It is also structurally important to recognize that this opportunity involves a mature, long-haul crude pipeline asset undergoing expansion. These types of infrastructure assets typically exhibit high operating leverage and relatively low variable costs, while generating revenue primarily through long-term, fee-based or take-or-pay transportation contracts. This structure provides stable and predictable cash flows with limited exposure to commodity price fluctuations, which can support materially higher asset EBITDA margins. To reflect this potential upside, we have also included sensitivity cases using 80% and 90% asset EBITDA margins in the aggregated model below. include the aggregated model for 80%, and 90% asset EBITDA margins below as well.

80% EBITDA Margin

90% EBITDA Margin

Putting it Together

That being said, we believe these two transactions serve as near-term catalysts for PPL’s share price, offering meaningful upside potential while also providing portfolio diversification benefits through a potential hedge against U.S.–Iran-related geopolitical risks. An escalation in geopolitical tensions would likely further incentivize the Canadian government to accelerate the development and expansion of domestic pipeline infrastructure. At the same time, the transactions provide investors with significant exposure to an active data infrastructure opportunity occurring outside of the United States.

While the specific timeline and transaction details remain relatively uncertain, the strategic rationale and underlying drivers supporting these projects remain compelling. As a result, we believe the probability of these developments progressing is sufficiently high to warrant consideration in the investment thesis.

Comments