Red Chris Block Cave - Imperial Metals

- 1 day ago

- 8 min read

Summary

Red Chris has undergone significant fundamental de-risking since the 2021 Pre-Feasibility Study, with improved technical confidence, resource potential, regulatory approvals, and government support positioning the project as a potential long-life copper-gold operation.

The project has the potential to materially transform Imperial Metals' valuation by providing exposure to decades of copper and gold production through its 30% ownership interest, while benefiting from Newmont's operational expertise and reduced financing risk.

The remaining value drivers are execution and cash flow realization, with the Definitive Feasibility Study, capital requirements, commodity prices, and free cash flow margins determining the magnitude of the potential market re-rating.

The Red Chris Block Cave is arguably the most important value driver for Imperial Metals (III:TSX). While the market has been aware of the underground expansion since the publication of the Pre-Feasibility Study (PFS) on October 11, 2021, the project's investment quality has improved materially over the past five years.

Rather than a single catalyst, Red Chris has experienced a sequence of risk reductions:

Technical feasibility established.

Resource confidence expanded.

Environment and Indigenous approvals secured.

Government financial support announced.

Definitive Feasibility Study (DFS) nearing completion.

Final Investment Decision (FID) approaching.

Originally, Red Chris was planned as an open pit mine with an expected operating life to around 2038. The open pit is contrained by economics: as the pit gets deeper, the amount of waste rock that must be removed grows rapidly, eventually making additional mining uneconomic. The block cave expansion chanes the underlying economics.

Instead of continuing to deepen the pit, Newmont plans to access the deeper orebody from underground using block caving, a bulk underground method that is well suited to large porphyry copper-gold deposits. This allows the operation to recover mineralization that would be prohibitively expensive to reach by open-pit mines.

Throughout this paper, we present a comprehensive de-risking narrative for the Red Chris Block Cave project, highlighting the fundamental developments that have materially improved its investment profile. We place particular emphasis on the recent mine-life extension and assess its implications for Imperial Metals' intrinsic value, including the potential per-share re-rating as the market incorporates these developments into its valuation.

Stage 1: Technical Validation

The first major catalyst occurred with the release of the Red Chris Block Cave Pre-Feasibility Study on October 11, 2021. The study demonstrated that transitioning Red Chris from an open-pit operation to an underground block cave mine could create a long-life, low-cost copper-gold asset with attractive economic characteristics. This marked an important shift in investor perception. Prior to the PFS, Red Chris was primarily viewed as a mature open-pit operation with a finite reserve life. Following the release of the study, however, investors began evaluating Red Chris as a potential Tier-1 underground copper-gold district capable of producing meaningful cash flows over several decades.

Despite the encouraging economics presented in the PFS, considerable uncertainty remained. Key project risks included environmental permitting, engineering design, financing requirements, Indigenous consultation, and uncertainty surrounding the final capital cost. Although the PFS substantially reduced technical uncertainty by demonstrating the project's viability, execution risk remained significant, limiting the market's willingness to fully capitalize the project's long-term value.

Stage 2: Resource Expansion and District Potential

Following the completion of the PFS, continued exploration and resource delineation further strengthened the investment thesis. Ongoing drilling, particularly around the East Ridge deposit and adjacent mineralized zones, indicated that the Red Chris mineral system was likely more extensive than originally contemplated. Rather than representing a single underground mine, the project increasingly appeared to encompass a district-scale copper-gold system with substantial long-term development potential.

This distinction is particularly important because mine life is one of the primary drivers of valuation for large mining assets. A longer operating life allows fixed infrastructure costs to be spread across greater production volumes, improves capital efficiency, increases project net present value, and provides management with greater flexibility to optimize production throughout commodity price cycles. Furthermore, a larger mineral inventory creates additional exploration optionality, allowing future drilling programs to potentially convert resources into reserves and extend mine life even further. Consequently, investors began viewing Red Chris not simply as an underground expansion but as a long-duration strategic asset with significant upside beyond the original mine plan.

Stage 3: Regulatory De-Risking

One of the largest uncertainties facing any major Canadian mining project is the permitting process. In June 2026, Red Chris achieved one of its most significant milestones when the Province of British Columbia approved the regulatory amendments necessary for the transition from open-pit mining to underground block caving. These approvals included amendments to both the Environmental Assessment Certificate and the Mines Act authorization.

Equally significant was the collaborative process through which these approvals were obtained. The regulatory process involved extensive engagement with the Tahltan Nation and culminated in a consent-based framework that substantially reduced social and permitting risk. From an investment perspective, this represented a fundamental shift in the project's risk profile. Red Chris effectively transitioned from a project that "may be built" to one that "can be built," leaving the primary remaining uncertainty centered on Newmont's internal investment decision rather than external regulatory approval.

Stage 4: Government Support

A further reduction in project risk occurred in July 2026 when the Government of Canada announced a C$500 million commitment to support the Red Chris Block Cave development. Although these funds are directed toward the project rather than directly to Imperial Metals, the implications for shareholders are nevertheless meaningful.

Government participation lowers the overall financing burden associated with constructing the project, strengthens project economics, reduces financing risk, and decreases the likelihood that Imperial Metals will require substantial shareholder dilution to finance its 30% ownership interest. Moreover, federal participation serves as external validation of Red Chris's strategic importance within Canada's critical minerals strategy, reinforcing the project's significance as a long-term source of domestic copper production. Government support therefore provides both tangible financial benefits and an important signal regarding the project's national economic importance.

Stage 5: Approaching of FInal Investment Decision

The final major catalyst remaining is the completion of the Definitive Feasibility Study. Unlike the earlier PFS, the DFS will provide a substantially higher level of engineering certainty by establishing the final capital cost, production schedule, operating cost structure, updated project economics, and construction timeline. These results will ultimately form the basis for Newmont's Final Investment Decision.

Historically, the transition from development-stage asset to approved construction project represents one of the largest valuation inflection points within the mining industry. Once financing, engineering, and execution plans are finalized, investors typically apply lower discount rates to future cash flows because project uncertainty has been materially reduced. Consequently, successful completion of the DFS and a positive investment decision could serve as the final major catalyst for a market re-rating of Imperial Metals' interest in Red Chris.

Valuation

Given these catalysts, we focus our analysis on the fourth catalyst, the Canadian government's recent financial support for the Red Chris Block Cave project. We examine how this commitment materially improves the project's financing profile and, under our assumptions, effectively reduces Imperial Metals' capital requirement from approximately C$540 million to roughly C$40 million while allowing shareholders to retain the majority of the project's long term economic upside.

Framework

In our base case, we assume total project capital expenditure of C$1.8 billion, annual production potential of 80,000 tonnes of copper and 316,000 ounces of gold. We apply copper pricing of US$13,540 per tonne, equivalent to C$19,148 per tonne, and gold pricing of US$4,095 per ounce, equivalent to C$5,791 per ounce, based on a USD/CAD exchange rate of 1.41. Additionally, we assume a project life of 14 years and apply a 10% discount rate, representing the midpoint of the commonly used discount rate range for valuing mining projects at the feasibility and development stages. This discount rate reflects the project's strong jurisdictional advantages, experienced operator, and government support, while still accounting for remaining execution, financing, and commodity price risks.

Base Case model

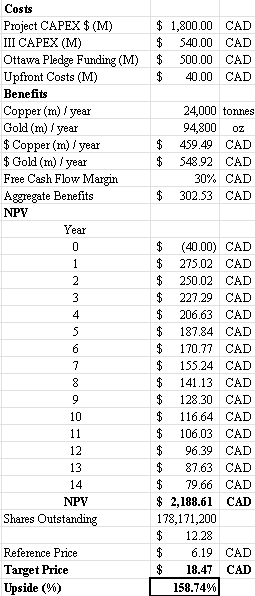

In our base case, the most important variable, aside from the assumptions established above, is the free cash flow margin, as it directly determines the project's ability to convert revenue into sustainable cash generation and ultimately drives valuation.

A 20% free cash flow yield assumption is reasonable for the Red Chris Block Cave project because it reflects a balance between the project's strong asset fundamentals and the remaining risks associated with developing a large-scale mining operation. Unlike a greenfield exploration project, Red Chris benefits from an existing operating mine, established infrastructure, a large copper-gold resource, and the operational expertise of Newmont as the project operator. These characteristics reduce development risk and support a higher valuation compared with typical mining projects.

At the same time, Red Chris is not yet a fully de-risked producing asset, as the block cave expansion still carries meaningful execution risks, including construction cost overruns, underground development challenges, production ramp-up risk, commodity price volatility, and Imperial Metals' financing obligations for its 30% ownership interest. These risks justify applying a higher expected return compared with mature producing mines, where cash flows are more predictable.

A 20% free cash flow yield represents an appropriate midpoint for a permitted development-stage mining project with Tier-1 characteristics. Mature Tier-1 producing mines may trade at lower free cash flow yields of approximately 8% to 15% due to lower uncertainty, while higher-risk development projects may require yields above 25% to compensate investors for greater execution risk. Red Chris sits between these categories because it has already achieved significant technical and regulatory de-risking but has not yet reached steady-state production.

Under this framework, a 20% free cash flow yield implies that investors are valuing the project based on its ability to generate substantial long-term cash flow while still incorporating a risk premium for the remaining uncertainties. This assumption appropriately reflects Red Chris's combination of a high-quality copper-gold asset, long mine life, experienced operator, and strategic importance, while maintaining a conservative approach given the risks inherent in large-scale underground mine development.

Since the free cash flow margin can vary significantly depending on the remaining risks discussed above, we present a scenario-based valuation model using a range of free cash flow margins from 10% to 40%.

Model: FCF Margin = 10%

Model: FCF Margin = 25%

Model: FCF Margin = 30%

Model FCF Margin = 35%

Model FCF Margin = 40%

Putting it All Together

The recent government support represents a particularly important milestone as it improves the project's financing profile and reduces a key uncertainty surrounding capital intensity. Combined with Newmont's operational expertise, existing infrastructure, and the project's strategic exposure to copper and gold, Red Chris possesses several characteristics typically associated with high-quality mining assets. The extension of the mine life into the mid-2040s further enhances the project's value by allowing the significant upfront investment to be amortized over a longer production period while providing Imperial Metals with decades of exposure to future commodity demand.

Our valuation framework recognizes that the ultimate value creation from Red Chris depends on several key variables, particularly free cash flow generation, commodity prices, operating performance, and Imperial Metals' ability to fund its 30% ownership interest. To account for these uncertainties, we apply scenario-based analysis across a range of free cash flow margins rather than relying on a single outcome. This approach reflects the inherent volatility of mining projects while providing a more balanced assessment of potential value.

Overall, the Red Chris investment thesis is centered on a multi-year fundamental re-rating driven by progressive risk reduction. While execution and commodity risks remain, the project has moved significantly closer to becoming a fully realized, long-life copper-gold operation. If the Definitive Feasibility Study confirms competitive economics and the project proceeds toward construction, the market may begin to recognize the substantial value embedded within Imperial Metals' 30% ownership interest, creating the potential for a meaningful re-rating of the company.

Comments